Latest articles

Understanding Regional Nuance: Return to Office Trends…

Are your employees happy with their expectations of working in-office? As financial institutions design their return to office frameworks, balancing…

From Hybrid to HQ: The Impact of Return to Office on…

Are your return-to-office mandates a cultural engine, or a potential talent drain?

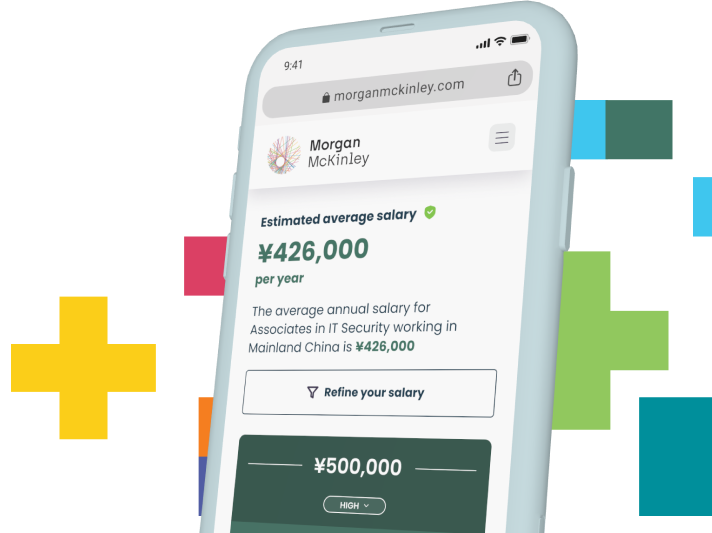

Your Guide to a Changing Financial Services Hiring…

Is your Financial Services recruitment reflective of what candidates want in 2026? Ensure your hiring is on the right track with our 2026 data on skill…

Considering a career move?

If you want to progress or even move into a new industry, browse our current vacancies to find your ideal job today.

VIEW ALL JOBS

Key In-Demand Jobs in Mainland China in 2026

Looking to make your next career move or simply want to know where your industry is headed? Understanding which jobs are in demand right now can…

10 Of The Highest Paying Jobs In Mainland China In 2026

After a challenging 2025, the 2026 employment landscape in Mainland China is entering a more encouraging phase of stabilisation and momentum.

Quality vs. Cost: 8 Strategic Hiring Lessons from the…

What can you do to ensure that you’re hiring top-quality candidates in a tight economy where budgets may be more constrained?

Preparing for your interview

Prepare, Review, Evaluate, PerfectMorgan McKinley has developed a tailored approach to preparing you for interview with clients –…

How to calculate a starting salary

You’ve identified that your company requires a new employee. This is an exciting time for you, the team they’ll be joining and the business as a whole…

Personal values vs company values

Check out this article from our Career Ally Hub to explore more details about personal values and company values

2017 Banking & Financial Services Salary Guide

Banking & Financial Services salaries across accounting and finance, asset management, operations, insurance, corporate & retail banking,…

Internet + Strategy in China

Since “Internet+” appeared in the government report by Chinese Premier KeQiang Li, it became the hottest topic in 2015. Not only because it was…

How to explain the reasons for leaving your previous…

You are about to leave your old job, or are on the verge of accepting a new job offer. There is one question that you better be able to answer – why do…

Interview speeches

As a form of verbal communication, a speech utilizes both spoken and body language to provide a clear and complete response to a specific question or…

The Importance of the Adversity Quotient (AQ)

Psychologists agree that, a person’s career success depends on their intelligence quotient, emotional quotient, and adversity quotient. When IQ is held…